Many Americans take personal loans every year. They use the money for debt payoff, car repairs, or home fixes. But one big question comes up fast. How much will you pay each month? That fixed monthly amount is your EMI. EMI stands for Equated Monthly Installment. It is the same payment you send every month until the loan ends. This payment covers both the money you borrowed and the interest charge.

In 2026, personal loan rates sit around 12 percent on average. Your exact rate depends on your credit score and lender. Knowing your EMI ahead of time helps you budget. It stops money stress later. This guide walks you through every step. We keep it simple. You can calculate by hand, in a spreadsheet, or with free online tools. We pull the latest rates from March 2026 data. No hard math needed once you follow along.

What Is EMI for Personal Loans?

EMI is a fixed payment plan. Each month you pay the same dollar amount. Part goes to the principal. The rest covers interest. Over time, the loan balance drops to zero.

Personal loans in the US work this way. You get a lump sum. You repay over 24 to 84 months. Most lenders use the reducing-balance method. This means interest falls as your balance shrinks. Some older loans used flat-rate, but reducing-balance is now standard.

EMI differs from credit card minimums. Cards let you pay any amount. EMI locks in one number. This makes planning easy. You know exactly what leaves your bank account each month.

Why Calculate Your EMI Before You Borrow?

You compare offers from different lenders. One loan might look cheap but cost more in the end. EMI shows the real monthly hit on your wallet. It also reveals total interest over the full term.

Rates change fast in 2026. Average personal loan rate stands at 12.26 percent right now for a 700 credit score and three-year term. Excellent credit gets closer to 11.81 percent. Fair credit sees 17.93 percent or higher. Calculating EMI lets you test different rates and terms. You spot the best deal fast.

It also helps with budgeting. You check if the payment fits your paycheck. Many people skip this step and feel stuck later. Do the math first. It saves headaches.

The Two Ways Lenders Calculate EMI

Lenders pick one of two methods. Each gives a different payment and total cost.

Flat-Rate Method

This simple way calculates interest on the full original amount every month. It never drops. You pay more interest overall.

Formula: Add principal plus total interest. Then divide by total months.

Total interest equals principal times annual rate times years.

Example: You borrow $10,000 at 12 percent for three years. Total interest is $10,000 times 0.12 times 3 equals $3,600. Add to principal for $13,600. Divide by 36 months. EMI equals $377.78.

Flat-rate is easy but expensive for you. Some auto loans still use it. Most personal loans avoid it now.

Also Read Best Personal Loans for Bad Credit 2026: Top US Lenders Reviewed

Reducing-Balance Method

This is the smart choice for borrowers. Interest recalculates on the shrinking balance. Your EMI stays fixed, but more money goes to principal each month.

Formula: EMI equals P times r times (1 plus r) to the power of n, divided by (1 plus r) to the power of n minus 1.

P is your loan amount.

r is monthly interest rate.

n is number of months.

This method saves you thousands in interest compared to flat-rate. Most US lenders use it for personal loans in 2026.

Step-by-Step Guide to Calculate EMI Manually

You can do this with a calculator or pen and paper. It takes five minutes.

Step 1: Write down three numbers.

- Principal (loan amount)

- Annual interest rate in percent

- Loan term in months

Step 2: Turn annual rate into monthly. Divide by 12 and move decimal.

Example: 12.26 percent becomes 12.26 divided by 12 equals 1.0217 percent. As decimal, 0.010217.

Step 3: Raise (1 plus r) to the power of n. Use a calculator for this part.

Step 4: Multiply that number by r and by principal.

Step 5: Divide by the same number minus 1.

Step 6: Round to nearest cent. That is your EMI.

Let us use real 2026 numbers. Borrow $10,000 at 12.26 percent for 36 months.

Monthly r equals 0.010217.

(1 plus r) raised to 36 equals about 1.442.

EMI comes out to $333.39 each month.

First month interest is $102.17. You pay $231.22 toward principal.

By month 18, interest drops to about $55. Principal paid rises.

Last month interest is under $4. Almost all payment clears the balance.

Total paid equals $333.39 times 36 equals $12,002. Total interest is $2,002. That beats flat-rate by hundreds.

Repeat for your own numbers. Change one thing at a time. See how EMI moves.

How Amortization Works in Your EMI

Amortization is the fancy word for how payments split. Early months favor interest. Later months favor principal.

You can build a simple table.

Month 1: Balance $10,000. Interest $102.17. Principal paid $231.22. New balance $9,768.78.

Month 2: Interest on new balance. And so on.

By the end, balance hits zero.

This schedule shows why early payoff saves big. You cut future interest fast.

How to Use an Online EMI Calculator

Online tools do all math in seconds. They are free on bank sites and comparison pages.

Step 1: Open any personal loan calculator.

Step 2: Type loan amount.

Step 3: Enter annual rate from your offer.

Step 4: Pick term in years or months.

Step 5: Click calculate.

You instantly see monthly EMI, total interest, and full payment chart. Many show graphs too. Change numbers and compare three loans side by side.

In 2026, tools update with fresh rates. They match what lenders quote. Try different terms. A 60-month loan drops EMI but raises total interest.

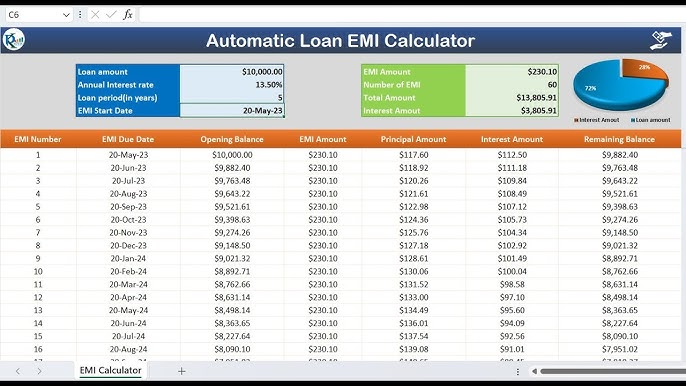

How to Calculate EMI in Excel or Google Sheets

Spreadsheets work great for US users. No extra apps needed.

Use the PMT function.

Type equals PMT(open parenthesis).

First number: monthly rate.

Second: total months.

Third: negative principal.

Close parenthesis.

Example for $10,000 at 12.26 percent over 36 months:

Monthly rate cell equals 0.1226 divided by 12.

EMI cell equals PMT(monthly rate, 36, minus 10,000).

Result: $333.39.

You can add extra columns for full amortization table. It shows every month split. Google Sheets works the same way and is free.

Save the sheet. Test new rates later. It becomes your personal tool.

Factors That Change Your EMI in 2026

Four things move your payment.

Loan amount: Bigger borrow means bigger EMI. $5,000 at 11.81 percent for 24 months equals $234.92 monthly.

Interest rate: This hits hardest. Excellent credit pays less. Current averages:

- Excellent (720+) : 11.81 percent

- Good (690-719) : 14.48 percent

- Fair (630-689) : 17.93 percent

- Bad (under 630) : 21.65 percent or more

A half-percent rate jump adds dollars every month.

Loan term: Longer term lowers EMI but costs more total. 36 months costs less interest than 60 months.

Fees: Origination fees of 1 to 8 percent raise effective rate. Always check APR. It includes fees.

Your credit score and income also matter. Strong profile unlocks lower rates.

Quick Comparison Table: EMI Examples for 2026

Here are real calculations using March 2026 average rates.

| Loan Amount | Annual Rate | Term (Months) | Monthly EMI | Total Interest Paid |

|---|---|---|---|---|

| $5,000 | 11.81% | 24 | $234.92 | $637 |

| $10,000 | 12.26% | 36 | $333.39 | $2,002 |

| $15,000 | 17.93% | 48 | $440.08 | $6,124 |

| $20,000 | 14.48% | 60 | $470.36 | $8,222 |

See the pattern. Higher rate or longer term changes everything. Use this table to test your own loan size.

Tips to Lower Your EMI and Save Money

Shop at least three lenders. Prequalify with soft checks first.

Pick shorter term if budget allows.

Add a co-signer with strong credit.

Enroll in autopay for 0.25 percent discount.

Pay extra principal when you can. Many lenders let you without penalty.

Check credit unions. They often beat bank rates.

Common Mistakes People Make

They forget total interest and focus only on monthly payment.

They use flat-rate math on reducing loans.

They skip APR and look only at interest rate.

They apply everywhere and hurt their score.

They borrow more than needed.

Avoid these. Calculate first. Then apply.

FAQs About EMI for Personal Loans

What does EMI stand for and why does it matter?

EMI stands for Equated Monthly Installment. It matters because it shows your exact monthly cost. You plan bills around it.

Can I lower EMI after I take the loan?

Yes. Refinance later if rates drop or your score rises. Or pay extra principal to shorten the term.

Do online calculators match lender numbers?

Yes. They use the same reducing-balance formula. Always double-check with your lender offer.

What happens if I miss an EMI payment?

Late fees add up. Your credit score drops. Some lenders offer hardship help. Call early.

Should I choose longer term for smaller EMI?

Only if you need breathing room. Longer term costs way more interest in the end.

Conclusion

You now know exactly how to calculate EMI for personal loans. Use the manual steps, Excel trick, or online calculator. Test different numbers with 2026 rates. Pick the loan that fits your budget and wallet.

Start today. Grab your numbers and run the math. Smart calculation leads to smart borrowing. You stay in control of your money. Better choices now mean less stress later. Go calculate your EMI and move forward with confidence.